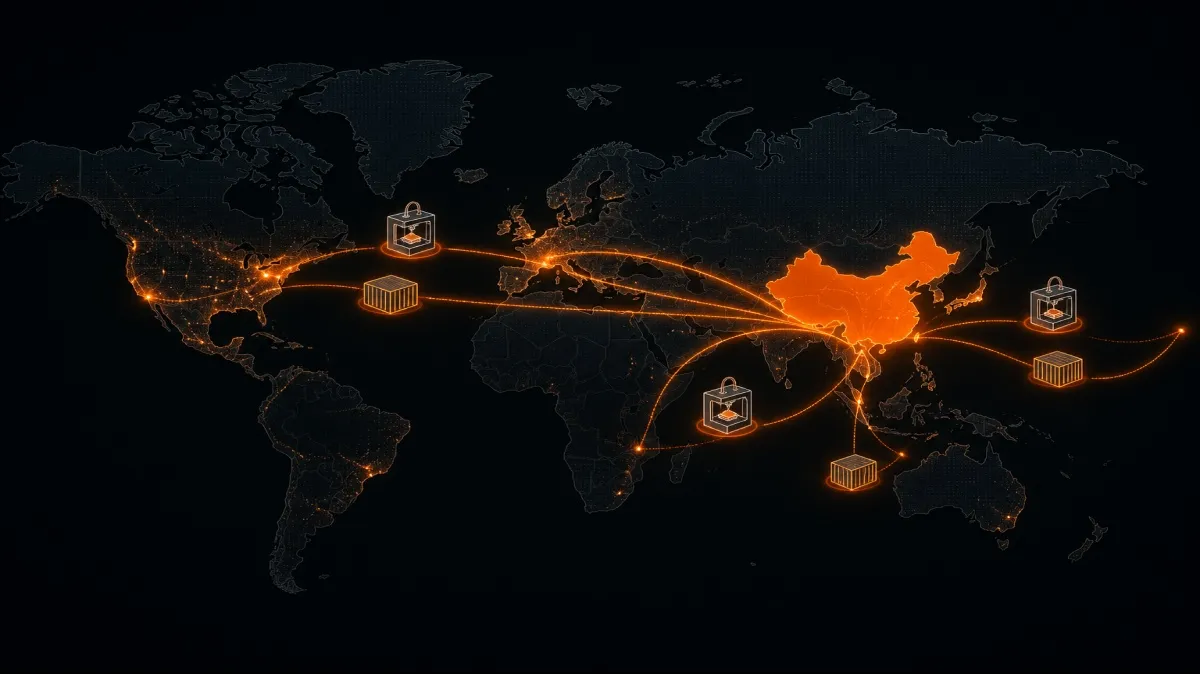

New customs data reported by Chinese state broadcaster CGTN shows that China exported approximately 2.46 million 3D printers during the first four months of 2026 — a year-over-year increase reported between 44.7 percent and over 100 percent depending on the source and measurement window. Whichever figure proves most accurate, the direction is unmistakable: China’s consumer and desktop 3D printing manufacturing base is scaling at a pace that has no real precedent in the industry’s history.

Shenzhen’s Outsized Role

According to the reporting, Shenzhen — in China’s Guangdong province — remains the epicenter of this growth, accounting for close to 90 percent of the global consumer-grade 3D printer market by some measurements. Shenzhen is home to an enormous concentration of the supply chain that makers around the world rely on daily: motion system components, stepper motors, hotends, control boards, power supplies, and the contract manufacturers that assemble finished printers for brands large and small.

This concentration is why so many of the brands familiar to US makers — Creality, Anycubic, Elegoo, Voxelab, and yes, Bambu Lab — either manufacture directly in or source heavily from the Pearl River Delta region. When Chinese state media reports a 50.9 percent year-over-year increase in 3D printing device production for the first four months of 2026, that growth is effectively the growth of the entire global desktop printer supply chain.

What’s Driving the Surge

Industry coverage points to a combination of factors behind the acceleration:

- Improved performance-to-price ratios that make Chinese-manufactured printers increasingly competitive even in markets where they previously struggled on quality perception.

- Expanded overseas sales channels, including direct-to-consumer e-commerce, regional distribution partnerships, and growing brand recognition outside China.

- Diversification beyond hobbyist FDM into resin printers, 3D scanners, laser engravers, and increasingly LFAM (large-format additive manufacturing) equipment aimed at small businesses and light industrial users.

This export boom is happening at the same time as major financial milestones for Chinese manufacturers — including Creality’s recent $1.12 billion Hong Kong IPO — suggesting that both capital markets and trade data are telling the same underlying story: China’s 3D printing manufacturing base has moved from “emerging” to “dominant” in the span of just a few years.

Why This Matters to the Community

Export volume statistics can feel abstract, but they translate into very concrete realities for makers shopping for their next printer, upgrade part, or filament spool:

- Bambu Lab owners are direct beneficiaries of this manufacturing scale. Bambu Lab’s ability to ship over a million printers a year — and to iterate quickly from the X1 series to the P1, A1, and H2 lines — depends entirely on the kind of high-volume, flexible manufacturing capacity that this export data reflects. A growing regional supply base generally means faster component sourcing for new product launches and potentially more competitive pricing on next-generation hardware.

- Creality and other budget-to-midrange brands face both opportunity and pressure. The same low-cost, high-capacity manufacturing base that helps them produce machines like the K2 and Hi series also lowers the barrier to entry for smaller, less established brands competing on price — intensifying the race to differentiate through software, ecosystems, and after-sales support rather than hardware specs alone.

- Prusa Research, manufacturing in the Czech Republic with an emphasis on European labor and supply chains, represents the clearest counter-example to this trend. As Chinese export volumes climb and price points fall, Prusa’s value proposition increasingly rests on reliability, repairability, open-source firmware, and a support model that doesn’t compete on raw manufacturing cost. Expect that positioning to become more pronounced in Prusa’s marketing as the price gap with Shenzhen-manufactured competitors widens.

- Voron builders and the broader DIY/open hardware scene are arguably the biggest indirect winners. Nearly every BOM (bill of materials) for a Voron 2.4, Trident, or 0.1 build sources critical components — linear rails, stepper motors, control boards, hotends — from the same Shenzhen-centered supply chains driving this export growth. Higher production volumes generally translate to better component availability, shorter lead times from sellers like LDO and BTT, and continued downward pressure on the cost of a DIY build relative to buying a finished machine.

The bigger picture here is a maturing global supply chain that increasingly underpins the entire desktop 3D printing hobby — regardless of which logo is on the front of your printer. As production scales in Shenzhen and exports climb, US makers can reasonably expect continued downward pressure on hardware prices, faster release cycles from major brands, and an increasingly crowded field of new entrants all drawing from the same manufacturing ecosystem. The challenge for established brands — and the opportunity for makers — will be in how that manufacturing capacity translates into actual product quality, support, and long-term reliability.

Source: Brand Official / Via FilamentPicks Automation